Register Company & Doing business Thailand – QA

129 Comments

Submit a Comment

Greetings,

We develop systems to serve more customers with reasonable fees.

Tana Sipa

Director and CPA

WhatsApp: +66 81.919.6225

Location: https://goo.gl/maps/MhJsbjkPrji51Qyt6

Services

Corporate Info.

Accounting – Tax Info.

Our Services

Corporate Services

- Company registration

- Vat registration

- change director

- change address

- change shareholder

- Increasing capital

- Decreasing capital

- Change company name

- Change Company seal

- Branch registration

- Change period of financial statement

- Company document search

- Notarization – Notary Public

- address for company registration

- Local Thai director service

- Opening company bank account

- Share Transfer Agreement

- Majority Shareholder Consulting

- Ready-made company for sale

- Company secretarial service

- Company Liquidation service

- Representative office registration

- Treaty of Amity – Thai & US

- Foreign Business License

- Foreign owned company registration

- BOI requiment and compliance

- Licensing application

- Incorporated document service

- Tax ID number

- Chartered Accountant

- Document Storage

- Land search, Title Deed search

We need help to either buy an old company or register a fresh start-up company. we also need a medium-size office to operate.

Yes, we have both option since we have more than 30 companies for sale from a few month to 8 years old, almost were registered for sale so there is no liability since we handle in tax, accounting and auditing for these companies or in case you prefer to register a new company we also can complete within 3 working days too, below is our guideline for new company setting up.

Can my condominium’s address be used for registering company?

The condominium can be used for registering company, but can’t be used for VAT registration. Therefore, you have to take into consideration if your company may need to register VAT or not. Basically, the company have to register for VAT when it falls into one of the condition as below;

(1)Earning annual income of 1.8 million Baht

(2)Company is partner with government

(3)Customer, partner or supplier or service provider required you to register for VAT

(4)When apply working permit for foreign staff

If 1 of the foreign director(s) and or one of the foreign shareholders of a current Thai company plans to open another Thai company (without the consent or knowledge of the other director(s) and shareholders), will there be any issues? e.g. tax, track records, bank issues?

No, there will be no issues with regards to the government, however, maybe there will be an internal problem (among the shareholders and or directors of the current Thai company), especially on the case if the new company that you would like to open has same business objectives with their company or if they don’t want you to open another company with other shareholders (without them).

Is that possible for 1 of the 2 foreign shareholders change to someone else later on?

Yes, can change to someone else later if you need, but the company need to have the director’s resolution for change of the shareholders’ list and also the director must approve and sign on the forms as well before can change the shareholders’ list.

Currently we are a company registered in Thailand and we have one customer in Thailand, A which we need to provide them rebate. Could you please advise us about this?

1) Rebate is not considered to be tax base for sales or service in accordance with section no.79 of the Revenue code. Thus, the rebate receiver does not need to collect 7% of VAT and no need to issue tax invoice when received the money (just issue the receipt).

2) Rebate is considered to be award/discount or any benefits in accordance with sales-promotion. Thus, a payer must deduct withholding tax at the rate of 3% when make the payment to a payee.

Rebate คือ ส่วนลดพิเศษทางการค้า ซึ่งอ้างอิงข้อมูลจากข้อหารือและคำสั่งกรมสรรพากรดังนี้ครับ เลขที่หนังสือ กค 0811 (กม.06)/พ.1095

Can we have online VAT user id and password for our VAT, so that we can file VAT online every month?

yes, you need to apply for user and password for tax e-filing, if you would like us to assist for this matter, we will charge Baht 3,210 (VAT included). Then, you can file VAT online every month (please note that the e-tax form is in Thai language only, however, you can compare with the English tax form which can be downloaded from RD website; http://www.rd.go.th/publish/29043.0.html.

Nature of Suspense input VAT (100650), A/R A/P Revenue Dept (100660), Tax deducted at source (100670) and Suspense output VAT (201460). Please clarify just to have a clear understanding on the nature of the listed accounts?

Suspense Input VAT /Output VAT

The VAT that is not filing yet because it is not due and recorded as suspense, and once we filing the VAT amount, it will be recorded as Input /Output VAT and cleared that Suspense Input /Output VAT.

A/R A/P Revenue Dept

It is VAT PP.30 of Dec’2018 and you have to be received as it is A/R and, but we will not request cash back, it will be offsets with Output VAT once you have it.

Tax deducted at source

It is the withholding tax amount that Client deducted us for the service that we provide and this tax amount can be used to deduct when the company has profit, but since it is first year and the company has loss, we can’t use that tax amount.

For closing company, during the step of VAT cancellation, we understood that the tax officer takes time to check back our company’s documents before he/she can finally approve and issue the VAT cancellation letter and send it directly to our company’s address. Moreover, while waiting for the said cancellation letter to be issued, our company is still responsible to continue the monthly VAT filing (which we can do online at RD system). Thus, for this mentioned, since our company has already terminated/cancelled the rental agreement with the address owner, the VAT cancellation letter (that the tax officer will send later) might just be thrown away by the said address owner and we would not be notified about it. Therefore, for this case, will this be a problem? Or is there any other way for us to know if the Vat has been already cancelled even without receiving the letter from the tax officer?

we have noted of your details and it will have no problem if the letter will be sent to your company’s address or if you did not personally receive it. Kindly note that there is another way to know if your company’s Vat has been already cancelled, which in case your side do the monthly VAT filing online and you cannot log in for the VAT on the system anymore, the VAT cancellation process has already been approved and is complete.

I have information that savings interest more than 20,000baht will be subjected to 15% withholding tax deduction.

Yes, the interest income received from all saving account for whole year is more than 20,000 baht will be subjected to15% withholding tax deduction.

I checked with bank and was told that only Thai national have condition of 20,000baht and all foreigners are subjected for deduction 15% regardless of interest amount.

Could you advise if above is correct as I could not find any information regarding withholding tax on savings for foreigners.

The interest income is the assessable income under section 40 (4) (a) in accordance with the Revenue Code of Thailand and under the Section 50 (2) (a) (http://www.rd.go.th/publish/37749.0.html#section50), it has been specified that the payer who paid this assessable income to a non-resident, (it does not mentioned as a foreigner) withholding tax shall be made at the rate of 15.0 per cent of the income.

However, refer to the Revenue Code Section 41 has specified that: Any person staying in Thailand for a period or periods aggregating 180 days or more in any tax year shall be deemed a resident of Thailand. Thus, due to you are the foreigner who residing in Thailand in accordance with the Revenue Code as mentioned and you are also the taxpayer and has paid the personal tax in Thailand. Thus, you should be considered as a resident in Thailand.

The tax officer has recommended that you may inform this information to the bank officer.

Can you please help to advice if our company will pay the accommodation to the hotel. Do we need to withhold any tax and at how many percent do we require to withhold?

The payment for the accommodation expenses to the hotel, resort or similar business is not subject to deduct for the withholding tax refer to the Revenue Departmental Order No. Tor Por 4/2528 Clause 12/1.

Our company registered for VAT , so for our every local invoice, it is required to include VAT 7 % for local projects. If international payment remittances transfer to us for the services provided for

the movie production of commercial to the Non Resident of Thailand, the 7 % of VAT still applicable on the invoice ? or its is exempted from VAT ?

Please note that if the service of movie production will be used in overseas only, the VAT will be added on invoice at rate 0%(refer to Revenue Code Section 80/1).

Moreover, in case such movie is produced in overseas and send direct to your customer in overseas, it will not be subjected to VAT (refer to Revenue Departmental Order No. Por 89/2542).

Under the law, could Thai companies issue tax invoices in English and under USD currency only?

Under the Revenue Department (RD) law, Sections 86/4, and 86/6, it states that:

Particulars in tax invoice shall be in Thai language, Thai currency and Thai or Arabic numeral. However, in some category of business which tax invoice is required to be in foreign language or currency, the VAT registrant shall be issue such tax invoice upon approval from the Director-General. 19

19N.DG.VAT.No.92, R.CT.No.25/2537

This means that tax invoices in other foreign languages and under foreign currencies is allowed, if only it could be prepared and issued together on 1 tax invoice with Thai Baht and foreign currency. For example, if client request for tax invoice in English and under USD currency only, it cannot be issued, which your company must issue 1 tax invoice with both the Thai Baht and USD currency together in one invoice.

Our Singapore company (head office) sold a software to our Thailand customer for their equipment updating. Thailand customer have deducted 8% from our selling price and remitted the balance to us. According to them, this is a form of Royalty under the DTA and they will provide us the Tax Certificate once received from the Revenue Department.

Please advise and confirm if such transaction is considered royalty under Thai Tax Law. I understand that we can claim from our Singapore Tax authorities but we did not enter any tax agreement with this customer.

Yes, this transaction is considered as a form of royalty under the DTA. Anyway, you could refer to the revenue department link for such matter as

http://download.rd.go.th/fileadmin/download/nation/singapore_e_revise1.pdf page 17 (article 12, item 2).

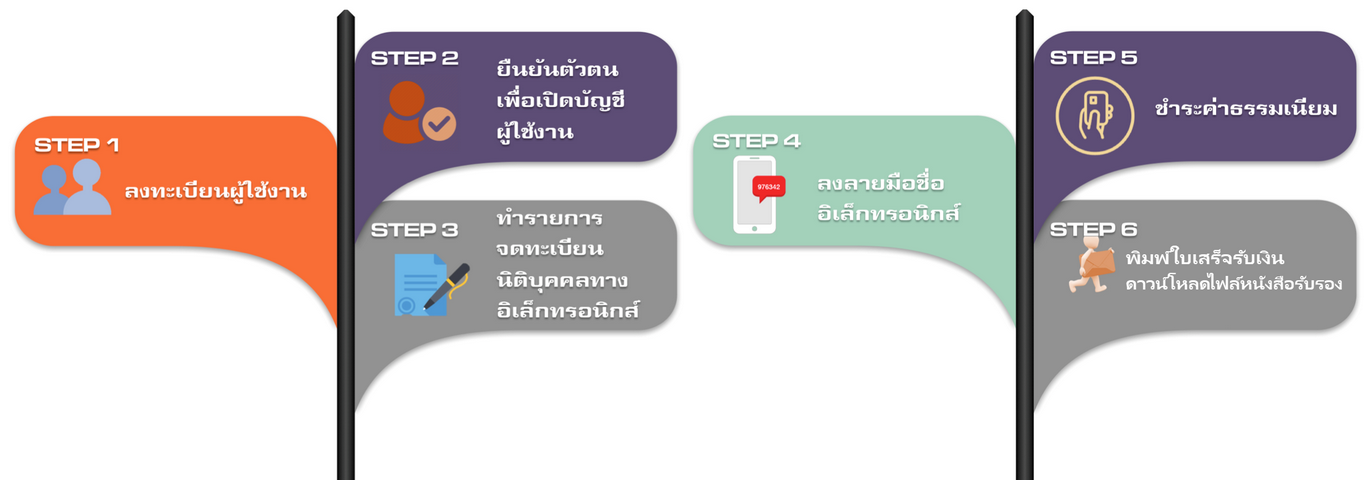

Do you provide company registration service under Treaty of Amity? If so, please let me know the cost and timetable.

Please see below for the sample time frame for your guidance.

Step 1 – Register the company +

VAT registration (if needed)

(at the Department of Business Development +Revenue Department)

time 3 working days

Remark – For this kind of service, all directors and shareholders must come to sign the registration forms in Thailand only

Step 2 – Request for Certification Under the Treaty of Amity (at the US Embassy), time 1 week.

Remark – The required document for this step is Notarized copy of American Shareholders and director’s passport.

(Can notarize at US Embassy)

Step 3 – Request for Certification Under the Treaty of Amity (at Ministry of Commerce), time 15 working days

Remark – The required document for this step is copy of all incorporate documents and copy of director’s passport

Is there any restrictions on American companies from importing sporting goods from China to sell in Thailand? That is my business, and I want to make sure it’s not a restricted activity.

There are restrictions on American companies, which there is no right to be protected under a treaty to operate a business following reserved activities:

(1) Communications

(2) transportation

(3) Fiduciary functions to take care of property for the benefit of others.

(4) Banking involving to deposit functions;

(5) Land ownership, exploitation of land or other natural resources;

(6) Domestic trade in native agricultural produces.

We would like to order a company search for a Thailand Company in English, which we need at least the name of directors, name of shareholder, kindly please advise if you could provide such service. If you can, please advise the price and the time required.

Yes, we can assist to search for the name of directors and the name of shareholders, but only Thai information is available so we will translate into English for you. Please visit our website at: https://www.panwagroup.com/companysearch.htm

With regards to the withholding tax, we have asked from our vendor which they insisted that the bill does not require withholding tax. In this case, can we just release the remaining outstanding to them? If there is any withholding tax required, can they handle themselves?

We recommend to check if the bill does requires to withhold the tax or not, due to if it is required to withhold the tax , the one who pays (the payer) is required by the law to deduct and file the withholding tax, so, the payer must be also liable along with the vendor (taxpayer) to pay the accrued withholding tax according to the Revenue Code Section 54.

We want to give a raise of 20.000 THB/month to our staff for his room rent. Please advise if it is subject for his personal income tax calculation or not?

Yes, the amount of Baht 20,000/month for his room rent is subjected for his PIT calculation. Please note that the assessable income that shall be considered as the benefit from employment and it will be subjected for personal income tax (PIT) calculation for example salary, wage, per diem, bonus, bounty, gratuity, pension, house rent allowance, monetary value of rent-free residence provided by an employer, payment of debt liability of an employee made by an employer, or any money, property or benefit derived from employment that pay to the employees as a fixed rate.

Please advise what is the expense that we will pay to our employees and it will not be subjected for PIT calculation. For example if we want to pay them for travelling or food when they travel for work.

The assessable income that shall be exempt for the purpose of income tax calculation are as: the per diem or transport expenses that an employee or a person performing work spends honestly, necessarily, exclusively and wholly in carrying out his duties (normally, it should have receipt or bill that the employees spent).

If our company has staff in Thailand, how long do we need to register it at social security and what is the SSO deduction for each staff. Moreover, when does SSO need to be filed?

Normally, if the company has the staff in Thailand, the company has to register Social Security Fund (within 30 days after employment) and for the calculation, the company deduct from the employee’s salary, 5% per month and another 5% from company (employer), totaling, 10% and submit it to SSO within 15 days of the next month.

Our company have account receivable – ABC, in amount of 16,000,000 Baht since year 2013 and it was recorded as allowance for doubtful account in full amount already from year 2016 to 2017, however, currently, the company cannot collect the payment from ABC, so how do you suggest to do for this case?

we propose you to write off this account receivable in year 2018 which it can be recorded to bad debt in full amount as following record:

Dr. Bad debt 16,000,000.00

Cr. Accounts Receivable 16,000,000.00

(To record the write of “account receivable” to “bad debt”)

2) Dr. Allowance for doubtful account 16,000,000.00

Cr. Bad debt 16,000,000.00

(To record reversing of “Allowance for doubtful account ” that was recorded in previous year)

Is my personal income in overseas (such as pension) be filed as personal income tax in Thailand?

Normally, this pension is subjected to personal income tax in Thailand when complete of these 2 conditions as below:

(1) You stay in Thailand reach 180 days a year in that tax year (calendar year).

(2) You bring that income to Thailand during the tax year.

In setting-up a private company, how much capital do we need to submit in the registration process?

Please note that there is no minimum required capital, but they require for minimum of 3 shareholders, (Baht 5 per shares), that means, you can start with Baht 15 capital, but we recommend you to start at least Baht 1 million due to the government fee of Baht 1 million or less than is the same.

What is the difference between Shareholder & Director?

Shareholder is the one who invest and hold the shares, but cannot sign any documents, but for the director, he or she can also be the shareholder or other different person, which all of the shareholders will appoint who can have the authorization on behalf of the company.

Our company has the expired goods and would like to destroy it. Please advise if we need to pay the sale vat for destroy product or not?

If the product has been destroyed in accordance with the procedures as mentioned in the Revenue Department Command Por.79/2541, these products shall not be subjected as selling goods according to the Revenue Code section 77/1(8) which shall not be subjected to submit the sales vat.

Our company will get the compensation income from supplier due to the problem from transportation. Please advise, if such compensation is subject to pay the sale vat or not?

Compensation income shall not be subjected as selling goods/services income according to the Revenue Code section 77/1(8), 77/1(10) and 77/2 which shall not be subjected to submit the sales vat.

The company has registered the VAT in Chonburi Province since January 2018 , however, the company has the plan to change the address to Bangkok on August 1, 2019. Moreover, the company has informed to The Revenue Department (Submit P.P.09 form for move-in ) on August 2, 2019, and put the date for move-in on August 20, 2019. Thus, when is the date that your company can issue the tax invoice under the new address?.

The company need to follow the date that they put in P.P. 09 form for move-in. In case, on the P.P. 09 put the date last August 20, 2019, so you can issue the tax invoice under the new address starting date August 20, 2019.

If the related company in oversea charge the management, coordination and bookkeeping to your company in Thailand, your company need to pay the tax?.

The company need to withhold the tax from overseas company if such service is used in Thailand at rate 15% (normal service) and file to Revenue Department and the Thai company need to file and pay VAT (7%) of such service to the Revenue Dept (instead of overseas company), however, Thai company can use such VAT as the company’s VAT credit.

If I have estimate net profit which will be paid the half year income tax exceeding from the actual income tax and my company have net loss in previous year, then how about the penalty?

The penalty is 1.5% per month of additional half year income tax, payable if the income tax from estimation of net profit exceeds 25% of the real income tax.

The company planned to pay the dividend on August 31, 2019, thus, does the company need to pay the tax for such matter?

When the company paid the dividend, your company need to:

1.Deduct WHT 10% from the amount of dividend payment

2.Submit the WHT form (P.N.D. 2) to The Revenue Department within 15 days of the following month (only online submission).

The Company is under BOI and paid the dividend to the shareholder on July 31, 2019. Does the company need to deduct the WHT?

When the Company is under BOI and paid the dividend to the shareholder, your company no need to deduct the WHT and submit the WHT form (P.N.D.2). Moreover, your company need to submit the summarized Dividend form (P.N.D. 2 Kor) to The Revenue Department within the end of January of the following year.

How much is the penalty charge that we need to pay if we delayed submit for the monthly VAT? Please advise.

In case delayed submission the monthly VAT. The company needs to pay as the following.

1) The fine for delay submission VAT return form = 300 baht within 7 days and 500 baht after 7 days.

2) Penalty is up to the amount of sale vat and there is also a surcharge of 1.5% per month of the tax payable.

What is the salary slip?

It is a detailed description of the employee’s benefit, deduction tax, social security, provident fund etc. and the net amount of salary payment for each employee.

For 1 Thai company, how many corporate bank accounts are allowed to be opened by the bank officer? Are there any restrictions imposed by the bank?

Normally, the bank do not have any restrictions as to how many corporate accounts you could open for 1 Thai company, however, the director or the company’s authorized person at the bank must discuss directly with the bank officer for this matter (such as the reasons and purposes why the company would like to open many accounts, etc.). The number of bank accounts that the company would be allowed to open would depend case by case on the approval of the bank officer.

In case the director of the Thai company is a foreigner, and he/she comes does not come to Thailand often, could he/she appoint the Thai shareholder of the company to be the authorized signatory on his/her behalf?

Yes, the foreign director can appoint the Thai shareholder of the company to be the authorized signatory for any related matters with the company’s bank account(s). For the process of appointing the authorized person, both the foreign director (who will appoint) and the Thai shareholder (who will be appointed) must be present together at the bank to sign the necessary bank forms.

Our Thailand company’s business is trading (local sale of raw peanut and chillies). For this matter, when we issue or do the local invoicing, do we need to add VAT and what are the possibilities of claiming too?

Please note that for raw peanuts and chillies (no further chemicals added or no other procedures done to the products), these are non-VAT or VAT exempted , as stated under Thai law, section 81 as :

Section 81 Value added tax shall be exempt on the following businesses-

(1) sale of goods but not for export purpose or provision of services as follows-

(a) sale of agricultural products whether they are trunks, branch, leaf, bark, offshoot, root, bud, bulb, pod, seed or other parts of plants and their by-products in fresh or preserved condition in order to temporarily prevent from spoiling during transportation by chilling, frozen means or by other means or preservation to prevent from spoiling for retail sale or whole sale by chilling, frozen, drying , grinding, segmentation method or by other method, white rice or by-product from rice milling but not including wood, firewood or products from wood sawing or food products in can container or package processed on manufacturing basis in accordance with terms and conditions prescribed by the Director-General.7

7N.DG.VAT.No.3, R.CT.No.23/2536

What is the income tax rate applicable for filing of PND. 51?

It is the progressive rate for the SME company which the paid up capital not exceeding Baht 5 million and the sale/service income not exceeding Baht 30 million, as below:

Tax exception for the net taxable profit not exceeding Baht 0.3 million

15% of the net taxable profit exceeding Baht 0.3 million but not over Baht 3 million

20% of the net taxable profit exceeding Baht 3 million

How do we determine if our company need to register for VAT? Do we have to report annually?

Your company may need VAT registration follow the below factors:

Your company generate income up to Baht 1.8 million per year.

Your customer or supplier request you for VAT registration.

To apply work permit for foreign staff.

To work with government sector or government university.

If your company does not fall under the above factors, you do no need to apply for VAT registration.

Remark; If you already register VAT, you must filing the VAT form (PP.30) every month, even though you don’t have any income. If you do not filing, it will have penalty charge every month.

Would it possible to increase the capital 10 million Baht and what are the documents needed to submit to the Government if increase capital for 10 million Baht?

Yes, it is possible to increase capital Baht 10 million, but please note that in case you increase the capital over Baht 5 million, the company must present the evidence of source of funds that shows the amount paid for shares which have 2 options as the below;

In case of investment by cash, the company must provide or present Bank certificate from the bank under company bank account showing the money as the same increase capital.

In case of invest by Asset, the company must provide the evidence as proof that they already transferred the asset to the company before registration for increase capital, such as if invest by the land, the evidence is title deed, must show the finished transferring of the owner already to the company, before we register for increase paid up capital at the (DBD)

Our business provides advertisement services to customers in overseas which such service will be used in overseas only, so, how about the VAT applicable to our service transaction and its supporting documents?

The VAT applicable is 0% of this service transaction and its supporting documents are Company’s invoice, customer’s PO/agreement, evidence of transferring service and evidence of using service in overseas only.

If we would like to open a private company in Thailand, and our mainly business is buying the wood from outside Thailand and sell to other country directly without passing in Thailand, would it possible to hold majority or 100% by foreigner?

Yes, you can register a private company by 100% foreigner and you can do the business immediately after open the company and no need to apply the FBL license (Foreign Business Act.)

Can you please advise if it is possible to convert our Thai company to a 100% Subsidiary of foreign company? Our main business activities are designing or creating and managing the conferment room, included to provide consulting services.

In case you need to hold by majority foreign owned or 100% by foreigner, your company need to apply the FBL license first (Foreign Business Act.), but please be informed that the government will allow to hold share only some business under annex 2 and 3 of Foreign Business Act (annex 2 allow to hold share maximum 75% and for annex 3 can hold 100%); for your case can apply under annex 3, due to your business scope is providing services, but it depends case by case and on the consideration of each officer.

our company just setting this year, so, when the income tax of company should be filed to Government?

Normally, the income tax of company will be filed 2 times per year; half year income tax which will be filed within 2 months after ending of 6 months of accounting period and annual income tax which will be filed within 5 months after ending of accounting period. Moreover, the first year of new company (just setting up) don’t need to file the half year income tax due to the accounting period is not complete 12 months.

What is Accrued withholding tax of PND.3, 53 account?

Accrued W/H P.N.D. 3 is when company pay service fee to a person,

Accrued W/H P.N.D. 53 is when company pay service fee to another company (juristic person)

Both PND. 3 and 53 must be filed within 7th of the following month. Moreover, when the company pay service every time, need to deduct the rate (depend on service paid).

Our company do consulting service business and have many tax sales invoices, but do not have tax purchase. Thus, for this matter, how will the company reduce sales tax to pay less revenue?

Please be informed that in case company do not have tax purchase, need to pay full amount of sales tax to RD, however if have tax purchase, can deduct with tax invoice sales in order to pay less tax.

Our company do business related to market (which opens only on weekends and holidays), and have income from subdividing rental space in our market; each rental space is not prepared as room and without partition. Thus, this kind of income is exempted from VAT?

This income is not exempted from VAT; if rental subdivide space did not have the proportion partition and did not have the door and it is also no delivery of possession to the tenant due to they can sell only on the date and time of opening and closing market.

For company setting-up, in case one of the shareholders is a family member and holds 1% , is his or her signature required? And any document other than passport required from him or her?

Yes, even though he or she holds only 1% still need to come to sign the documents in Thailand. Moreover, for the required document and/or information, aside from the passport, we need his/her address in overseas and contact number as well.

I have heard many bad stories of farang going back to home country for holidays and when they return to Bangkok, the corporate bank account is empty because Thai shareholder has removed all funds. What protection or guarantee document do I have to produce to make sure the Thai majority Shareholder cannot take money out of the corporate bank account?

Normally the majority shareholder cannot take any money out, only the director (who normally is the authorized of the company’s bank account and who had opened the account) can withdraw out the money, because the shareholder cannot sign any documents including the documents related with the bank. Maybe the bad story from others is that they have Thai director and not the shareholders or the foreign director gave power of attorney to some Thai to handle of all business on their behalf, but if you are only one director, so, they cannot take out your money.

The company provides annual company trip for employees, which the company purchases a tour package. Moreover, the tour company will issue a full tax invoice to be used to claim back VAT?

Yes, the VAT purchase can be used to claim back VAT, which the company must present the tour package under welfare of employees.

The company needs to sell the company car, but don’t know the potential price for selling. Please advise.

The company must sell cars follow market prices and also must include VAT 7%.

Our Thai staff have loaned amount of Baht 100,000 from our Thailand company. For this matter, does the company need to charge interest rate? Yes or No?

Normally, the company can decide to charge interest or not, which if charge, company could also decide on how many percent will they charge for the interest rate. However, if the tax officer random checks the company, they have the right to evaluate and inform the interest rate directly to the company, depend on their decision.

For the tax forms in Thailand, is it compulsory to be submitted in Thai version or the company can submit in English version?

Under the Thai law, your company need to submit the tax forms and related documents in Thai version only.

Can I buy the ready-made company and leave it inactive until I am ready to start to do the business ?

Yes, you could buy, then can keep the company inactive first like dormant company until you are ready to do the business. Anyway please be informed that although inactive (dormant status) you still have to submit some kind of tax return such as corporate income tax (PND.50), half-year tax (PND.51) and VAT form (PP.30, if any) and also audited financial statement. Further information of its submission you can call our office at +66 2933 9000.

The foreign company already got the license from MOC under Foreign Business Act.(FBL) following their current business objective(s), however, the next 3 months, the company decided that they still need to have more business objectives which are different from the current business that already obtained the license, thus, could the company do the new business directly or how the company can do the business?

If in case the company need to do more business and different with the one that the company obtained the license, the company must apply the license under the new business first before start the new business, and in case already start the business, must also hurry up to apply the license before the officer will random check. If in case the officer check and found out that your company have not yet apply the license, you may have to pay penalty charge or they will do the legal process or worst case maybe the license will be revoked or Ordered for dissolution.

Regarding the tax invoice preparing, the company can run the number of tax invoice by number of month (such as May; 05/001) and running number by category of client (such as trading; T0001), right?

Yes, you can, however, the detail of tax invoice should have at least items according to the Thai law and the tax invoice should have running number (not cross or skip).

I am a Singaporean; I already have a company in Thailand and I want to open a corporate bank account under this company. Anyway, I am not convenient to come to Thailand. Therefore, to resolve this matter, since there is a Bangkok Bank branch in Singapore, is it possible if I sign the bank documents in the presence of an authorized bank officer at the Bangkok bank branch in Singapore?

For this case, you actually cannot sign in the Singapore branch, but you could discuss directly with both sides (the bank branch in Singapore and the bank office manager in Bangkok bank Thailand) if they would allow for this matter or not, due to some case they allow and some case they do not allow.

Next year, I plan to decrease the company’s capital (from 10 million Baht to 2 million Baht). Is it possible if you can assist all steps to finish within the next year?

Yes, we can assist for this matter. Moreover, please be informed that normally for decrease capital, it can be done not more than 6 times within 1 year and can decrease not more than 75% per time (like 2 months can decrease capital 1 time) only.

The objective of company is maintenance service of audio equipment. How about the tax points of my business?

The business of maintenance is fall into service type, so tax points of VAT for a service business are when the fist coming between:

1.we get paid from client or,

2.issue the Tax invoice to clients

The objective of company is trading of audio equipment. How about the tax points of my business?

The tax points of VAT for sale goods is when coming first between:

1.we deliver goods to customer or,

2.get paid from your customer before delivery of goods or,

3.issue the Tax invoice to clients

After our company has been liquidated completely, we will return the capital and retained earnings to shareholders, does the company need to withhold the tax from it? And how much is the withholding tax rate?

the company should withhold the tax from the part of returned money that exceed from shares capital (purchase price), if shareholders are personal; withholding tax rate is progressive rate except they are not resident in Thailand; withholding tax rate is 15%, if shareholders are juristic person that are incorporated according to the law in overseas and they did not operate in Thailand ; withholding tax rate is according to Revenue Code section 70.

My bosses want to know the Thai Law on publishing in the local newspaper for invitation of the annual general meeting. Can you provide us the information on this matter?

Regarding the process of AGM in accordance with the Thailand law.

We would like to refer to the Civil and Commercial code: Limited Companies (section 1175).

Section 1175 Notice of General Meeting

Notice of the summoning of every general meeting shall be published at least once in a local paper not later than seven days before the date fixed for the meeting, and sent by post with acknowledgement of receipt to every shareholder whose name appears in the register of shareholders not later than seven days or, in case the notice is for a special resolution to be made by the general meeting, fourteen days before the date fixed for the meeting.

Our company must make the payment to our suppliers and they requested us to deduct the withholding tax and have requested us to prepare the withholding tax certificate to them as well. Could you please explain to us “the amount paid” and the “amount of tax withheld” that we need to fill-out on the said document

The “amount paid” that you need to fill out in the certificate of withholding tax is the amount of expenses (before VAT).

The amount of “tax withheld” that you need to fill out in the certificate will calculate from the amount paid at the rate of 1%, 2%, 3% or 5% are depend on a type of income that you must pay to them.

With regards to the company address, right now, we are on the process to discuss with the landlord to provide the relevant documents. Moreover, we have one more question about the lease agreement, which is: When making the lease agreement, what parts do I need to be careful?

Do a Thailand registered company need to maintain a statutory records such as Register of Director, Register of Shareholders etc

The Shareholders’ list must be uploaded to DBD within 14 days from AGM date, but for Director there is no requirement.